It’s rarely easy for angel investors to figure out which startups are worth the time and investment.

Once you’ve built a reputation as an active and trusted investor, you may find yourself buried under a vast number of approaches, all which require you to do due diligence research or to spend an inordinate amount of time filtering out low-quality deals.

Often, you are left trying to assess whether you’ve got a great investment opportunity in front of you or simply, a great idea or a founder who’s great at pitching.

The reality at Investible is that we review more than 100 startups for every one investment we make. And it’s by having a strong process and proven investment methodology that we’re able to maximise the chances of successfully identify the 1% that make it all the effort worthwhile.

When assessing a startup, we first want to understand the ‘health’ of the business – well before we start thinking about a potential deal.

Here are the four areas we drill into with an early-stage business and how investors can improve their own due diligence process:

1. Who you’re dealing with: The founder (and broader team)

Riderless horses don’t win races and while there are exceptions, inexperienced riders are less likely to have a podium finish. A quality founder or founder team is crucial a startup’s success, especially early in the race. That’s why we focus on the founders first.

Investors need to consider the founder’s passion, resilience, experience and skills, especially when it comes to the problem the startup wants to solve, as well as their unique attributes, attitudes, values and vision for the business. Generally, we find that startups are more successful with more than one founder, so the assessment should also consider the synergy, complementary traits and gaps across the entire founder team.

As a business grows beyond the founders, the ultimate scalability will largely be determined by its wider team of employees, partners and supporters. Investors should assess the depth of experience and quality of this extended team, and indeed, the founder’s ability to attract and motivate great talent to their vision for the business, especially in later raises.

2. What you’re dealing with: The business model and traction to date

The business model is the foundation of a growing business, but it is often the factor that startups don’t spend enough time thinking about and validating.

Hugh Bickerstaff, Global Head of Investment, Investible. Photo: supplied

There are three essential ingredients in a strong business model – the value proposition (desirability), the delivery proposition (feasibility) and the financial proposition (viability). It’s important that the founders be able to explain how they’ve validated their decisions in each of these areas.

For more established businesses, traction is a great indicator but investors should remember traction is assessed differently for early-stage companies.

For startups, consider the recency of what has been achieved, under what conditions and with what resources. The earlier the business, the more important the quality of the traction as opposed to the quantity. In any case, investors should consider whether the traction is trending in the right direction and if it is scalable in a bigger arena.

Founders must also keep in mind that markets differ by geography, so if your plan is to make it big in another country, such as the US, remember that investors will want to see validation specific and relevant to that geography or market.

3. What they’ve got: Plans, projections and assets

Once you establish that you like a business, it’s time to dive into the strategy and numbers. You’ll want to see evidence of a well-thought out game plan as businesses often run out of funds before they can raise more capital or become cash flow positive.

Consider whether the upfront capital investment, cash burn rate or cost of acquisition (CoA) is too high or financial models are based on one-off sales as opposed to showing opportunities for recurring revenue or a low CoA. And keep an eye out for projections that are not validated or founders who have forgotten to factor in key costs.

The stage of a business will determine how far you can drill down into the intangible and physical assets. Startups rarely have significant assets compared to later stage ventures, so this might not always be obvious. Assets could be the comprehensive nature of their tech, the incredible user experience, the size of their database or the dynamism of their branding.

In later stage businesses, it might include their goodwill and physical assets such as offices, hardware and contracts. It is also important to confirm the business’s current and proposed liquidity position before committing.

4. Who else is in the game: The competitive landscape and market conditions

A startup might have a great business model but what if someone gets there first, an overseas leader enters the market or that lagging corporate behemoth decides to wake-up?

If the gamble is to pay off, the business needs to be able to outmaneuver the competition.

There are a number of factors that might impact the startup’s future, from their execution, founders, the technology, their PR and marketing, the broader market and more.

Founders should demonstrate an understanding of the potential internal and external ‘threats’ and how they plan to overcome them – whether through their speed to market, their features or execution.

The industry and the timing of the startup’s entry into that industry is also crucial. Is the startup in a one-horse race (a “winner-takes-all” opportunity) or part of a growing market where greater competitor activity shapes the course for all players?

Consideration should be given to the potential barriers to entry specific to the startup’s industry and whether it is a sunrise (emerging) or sunset (diminishing) industry.

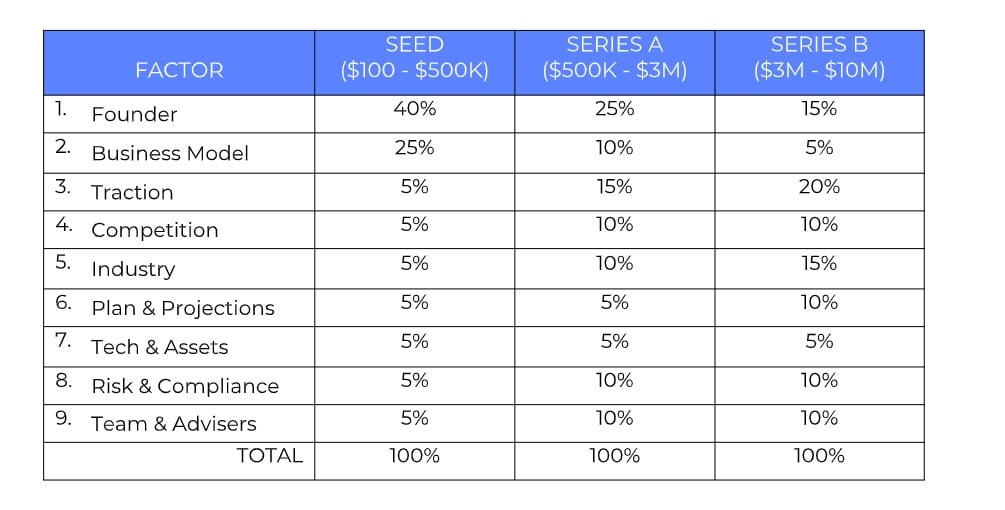

Weighting the key factors

The relative importance of these factors will differ for each deal depending on the stage of the business, the size of the deal and the preferences and goals of the angel investor.

In general, however, we weight the founder much more heavily in the early-stages, followed by the business model and then the remaining factors.

For Series A or Series B rounds, the weighting shifts more toward the traction and is more evenly spread across other factors such as the industry, competition, risk, projections and team.

It can be easy for investors to get caught up in a great pitch.

By setting a clear methodology for evaluating early-stage companies, investors can increase their chance of building a successful portfolio while also better managing the workflow associated with thorough due diligence.

- Hugh Bickerstaff is Global Head of Investment, Investible.

Trending

Daily startup news and insights, delivered to your inbox.